AES Galabovo (ME1) and ContourGlobal Maritsa East 3 (ME3) have been the subject of increased media attacks since the beginning of 2020. A month earlier – in December 2019, the Association of Industrial Capital in Bulgaria /AICB / initiated a petition against the so-called “American” TPPs. If you google ‘’AICB’’, “American TPPs” and “2019” on the Internet, you will find that last year’s references alone were 4,300 times, and the overall result is more than 37,000 times. The claims of this organisation were backed by some of the nationally represented employers’ structures and widely covered by the media. This was commented by economist Krassen Stanchev in an analysis for Trud Daily.

We publish the main highlights from the expert’s position of the role of so-called American TPPs – AES Galabovo TPP and ContourGlobal Maritsa East 3 TPP – for the energy sector and the economy of Bulgaria, for the huge investments that have made them the most modern and ecological capacities not only in Bulgaria but also on the Balkans, as well as for the permanent pressure that their investors have been subjected to by politicians and employers’ organizations for years.

Even the headlines show that there is an evolution in the messages. The only permanent thing is the subject matter, the referred TPPs dubbed enemies.

The evolution of the arguments against

The employers’ organization that back up the AICB point out that

(a) these two power plants are not being ‘burned’ by the high electricity prices (like everyone else’s) and

b) at such high prices, more investment should not be expected.

However, there is no comparison between the ‘savings’ from the eventual termination of the agreements with ME1 and ME3 with the costs of cancelling them and the adverse effects.

In 2014, the then SEWRC set a precedent in the EU’s work by lodging a request with the Directorate-General for Competition whether the previous decisions of the Bulgarian government on ME1 and ME3 were inadmissible state aid. In the list of closed similar cases, there is no instance in the DG where a Member State’s institution asks (and accordingly a procedure is opened) concerning a decision passed by another institution of the same country. Since then, there seems to be no development on the procedure in the Directorate. The above mentioned employers’ organisations, judging by the publications, are becoming more active on the topic after mid-2015.

There are three sides to the evolution of the arguments – rhetorical, thematic, and factual. The rhetoric, for example, has the tendency to use slang and vernacular. It has been especially evident in the last four months.

There are ten topics, that change somewhat and follow this timeline.

1. In the end of July 2014, immediately after the SEWRC demarche in Brussels, trade unions and employers want the government to nationalise the TPPs; it is said that the agreements are not transparent but they are not made public (this occurs at the same time with the privatisation of the EDCs) and there is a period of temporary silencing of the accusations.

2. In July 2015, a bill on the nationalisation of ME1 and ME3 was tabled to the National Assembly, sponsored by Valeri Simeonov who says: “Soon we will proof the unlawful state aid for Maritsa East 1 and 3.”

3. The bill is a translation of a Polish law of 2000 designed to clear property before privatisation; this is happening in 2002 (before that, in 1998, access to electricity transmission infrastructure, already “connected” to that of Central Europe and the EU, has been liberalised), and the labour force in the sector is cut from 400,000 to 150,000 people, but even after 2003, the subsidies for the energy sector remain; the difference is that this is considered permissible even by the radical “greens” in Bulgaria.

4. Without referring to these important prerequisites, the motives behind the bill, citing Poland, demand that the agreements be terminated immediately. This bill, as well as the 2014 requests, do not refer to the other coal-fired power plants and other power purchase agreements, but only the ‘American’ ones.

5. Then the Polish experience is forgotten for two years to reappear in the requests made in the first week of 2020, again without mentioning the important details;

6. In 2017, a new topic emerges – EU decarbonisation policy, which is being interpreted (again by employers and some government experts defending the Belene NPP project, not the Green) as a reason for closing ME1 and ME3. An important fact is overlooked mentioned in the estimates made by Georgi Bosev and Ivan Arseniev for the BAS Report on the state of the energy in the current year, that 70% of the currently installed capacity could operate until 2035, and 53% until 2040 under the standards in force at the time and provided the pollution standards and prices remain unchanged.

7. In the spring of 2019, a new “accusation” is made – the two TPPs are making big profits, which is repeated again at the end of the year and in the publications from the beginning of this year.

8. In December 2019, the proclamation is made for the termination of the agreements with ME1 and ME3 before the launching of the capacity mechanism tenders. The investment in ME3 is considered to have been repaid, although this is controversial in principle and it is very likely that it will be proven wrong in a lawsuit. This would mean shutting down the TPP, with eventual negative effects on Maritsa East Mines, fiscal risk and the risk of lost litigation.

9. On January 3 this year, an attempt is made to prove that because of the „American power plants” electricity in our country is more expensive than other EU countries and to calculate the amount of the “inadmissible” state aid per megawatt hour.

10. A new idea emerges – the budget to pay for the agreements with ME1 and ME3. This idea is formulated as follows:

a. “If the state does not have the will and the courage to put an end to this unlawful state aid, this robbery, let it pay for it from the budget and not burden consumers with expensive electricity”;

b. “Not to contribute to the deterioration of the competitiveness of respectable business and to suppress economic growth and people’s incomes”;

c. “And because the state does not have its own money (it is collected from all of us, the taxpayers), it can obtain it by reducing the over-staffed state and municipal administration and by restraining theft.”

This review does not include sporadic attempts (in 2018) to present bills as household expenditure (which is clearly incorrect) and the usual reference to the “Ivan Kostov government”. It is important because it is related to the nature of the agreements and the “inadmissibility” of state aid. “Integrity/good repute” is also a constant theme, but only as a suggestion that these two power plants are lacking in it and the occasionally accusation of “indecisiveness” of the government.

By the way, if the agreements were “to be paid for by the budget”, then we would have the case of pure state aid. But this is not the case.

What is the actual situation?

Obviously, some topics are recurring, and there are attempts to substantiate some claims with statistics. Significant repetitions are allegations of “unlawful state aid” and “repaid investment” of ME3, “expensive electricity”, “loss of competitiveness” and “big profits”.

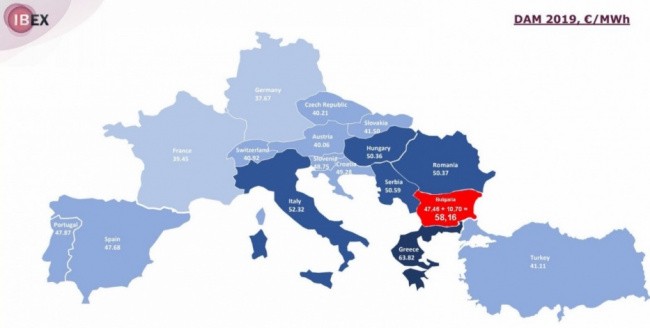

The ‘highest’ price

As an illustration of the ‘fact’ that the electricity prices are the highest is the following chart for 2019 for the day-ahead market on the Independent Bulgarian Electricity Exchange (IBEX).

It is evident – and this is a correct comment in last week’s publications, that for last year this market segment in Bulgaria had the highest price, with the exception of Greece. However, there are some subtleties that have not been taken into account. In the first place, the fact that the day-ahead market only deals with quantities of electricity that are not part of the long-term over-the-counter (OTC) agreements is not taken into account. According to various estimates, IBEX’s day-ahead market volume is about 30% of the total contracted quantities. This feature is noted in the following chart.

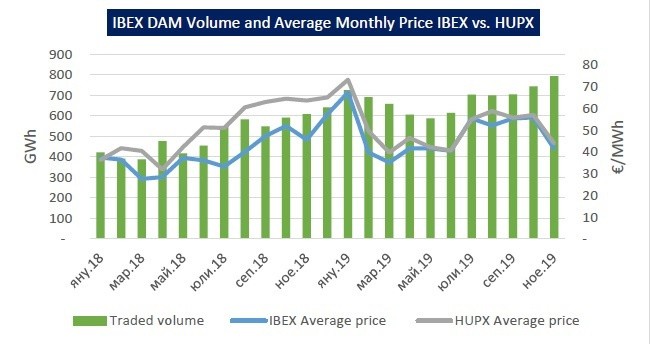

Delivered quantities and average price at IBEX (2018-2019)

All trade has been reported since 2018, following a corresponding change in energy law. The chart shows that the average price is lower than the day-ahead by about 10% over a long period of time.

An interesting comparison of the day-ahead market is with a country similar to Bulgaria. The following chart makes a comparison between the Hungarian Energy Exchange (HUPX) considered to be the ‘reference’ one for the region.

Day-ahead trade, Bulgaria – Hungary (2018 – November 2019)

The day-ahead price trend is practically the same since March 2019. For the previous part of the period it is on average about 10% higher in Hungary, including the cold January 2019.

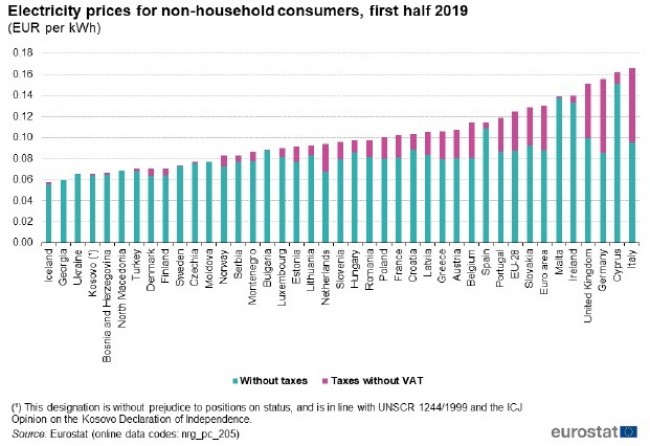

If we compare the prices for industrial consumers, which should be quoted in the above opinions on ME1 and ME3, in the first half of 2019 (this is available data from Eurostat), the situation becomes clear from this chart.

Electricity prices for non-household consumers in the EEA and countries acceding to the EU (January – June 2019, EUR/kWh)

Competitiveness

In fact, there should not be a problem with competitiveness. Or, if there is such, the reasons should be sought elsewhere. The differences between prices for industry and households are much more significant in the countries that have the most ambitious plans to restructure their energy sectors towards carbon neutrality. For example, in Germany in 2019 the price for industry is 3.6 times lower than the price for households. For Bulgaria, with a policy of maintaining a low ratio between household and industrial electricity consumers, it is difficult to finance technological innovations in the sector. The reason is that the basic equipment for electricity is supplied at market prices, which are formed in countries with other policies. Pricing policy such as that in Germany has the following positive economic implications:

– it allows for lower transition costs;

– encourages households to become aware and their service providers to deliver more energy-efficient appliances and/or services;

– less-affluent households do not finance the electricity consumption of wealthier households;

– prices allow producers to self-finance restructuring, transition costs.

Household prices

According to a review of electricity prices from April 2019 by the Energy Management Institute, the following is evident for Bulgaria for the period 2007 to 2018 Bulgaria.

– Electricity prices increase by about 1/5 less than the prices of other goods and services;

– This is an indicator that there should not be any significant negative effects on household consumption and this is evidenced by the dynamics of food expenditure in household budgets;

– Electricity production prices go up while prices for network services decrease;

– Network services reach their highest level for the period of 194 BGN/megawatt hour in 2012, then remain at a lower level;

– Regulated prices for the period July 2018 – June 2019 are 6 BGN/MWh lower than the prices in 2012.

For these and other reasons, Ivanka Dilovska from the Energy Management Institute believes that electricity prices will surely only go up in the coming years.

“Big profits”

Here again there are some important details that are missing.

The first one is that the net profit of the AmericanTPPs is not fixed but it depends on their management. By the way, it should be borne in mind that we cannot expect to attract foreign investors in the energy sector under such restrictions. The only prospect of making a profit is through administrative redistribution of the market and cross-subsidisation, such as Varna TPP in 2019. However, employers’ organisations and CITUB are not paying attention to it. The second is that ME1 and ME3 are compared with enterprises (with correctly cited data from the reports in the Commercial Register), that do not pay off investments.

The correct calculations should be made using the return on assets indicator, for the simple reason that the agreements with the two power plants are exactly to this effect. Then we would come with the following:

• Both companies are indeed among the top 20 in the country in terms of asset size in the Capital Top 100 ranking;

• ME1 ranks 9th in terms of assets (BGN 1 968 million), ME3 ranks 20th (BGN 962 million), while the average assets of an enterprise in the category are 1 300 million. BGN;

• ME3 ranked 8th (10.03%) and ME1 ranked 21st (4.79%) in terms of asset return, while the average amount was 4.16%;

• More profitable than ME3, but often with much more modest assets are Telenor Bulgaria, Euro Games Technology, Solvay Sodi, Huevepharma, Aurubis Bulgaria, Arsenal, Fraport Twin Star Airport Management;

• Ahead of ME1 are Energo-Pro Networks, Rompharm Companies, Agropolychim, Assarel Medet (with 40% less assets), Jumbo ES.B, Air Traffic Control (similar to Assarel), Bulgarian Telecommunication Company (with about 25% less assets paid), Bulgarian Energy Holding (with 2.5 times larger assets), Thrace Glass Bulgaria (with about 2.5 times smaller assets), Sopharma, Kaufland Bulgaria and Kozloduy NPP ( 1.7 times more assets already paid).

A similar analysis was also presented in November this year by Prof. Georgi Kaschiev.

“Paid off investment”

By leaving aside some of the real investment in ME3, one can conclude that the initial investment of around EUR 700 million (previously updated several times) has already been paid. The leaving aside should concern the investment processes, mainly in response to changing environmental requirements ContourGlobal Maritsa East 3 (ME3 is the first TPP on the Balkans to operate in full compliance with European standards on occupational safety and environmental protection). The TPP started operating in 2009. Additional investments were made in the period 2011-2015. Their total volume at the end of 2018 is about BGN 1.4 billion. It would be unscientific fiction to assume that it can be paid off in such a short period.

In the meantime, it should be borne in mind that the value added generated by the company on its own account, according to the reports for the period 2003-2018, is BGN 4.2 billion, and the total amount of indirect added value (generated by ME3 providers) for the period is BGN 764.1 million.

In the scenario of termination of the agreement with ME3, which is urged to be implemented immediately, there would be irreversible losses to the budget and the economy, including losses of suppliers, lost profits for the company and jobs, foreseen from the shutdown of the thermal power plant.

“Inadmissible state aid”

The AICB statements set out data based on the current EWRC Decision (p. 57) on the uncompensated costs of the two power plants, and then distinguish between other similar costs. In this context it is not mentioned that the two power plants reduced the cost of availability in 2016, as a result of which NEK reduced its expenditures by nearly BGN 100 million per year. When the uncompensated costs of all other power plants with similar agreements (RES, cogeneration, etc. – also correctly mentioned in the publications) are taken from the same table of the Decision, the amount over BGN 1.3 billion is obtained. There is no protest against these BGN 1.3 billion. The argument given is that they are under EU policy, whereas for ME1 and ME3 there is no such policy. This statement is also untrue: in the period when the agreements were signed, there were standards in place in the EU; the investments in ME1 and MI3 is to make Bulgaria meet these EU energy standards. Additional investment in ME3 is also a response to such a policy.

This means that it is correct to compare the 700 million with BGN 1.3 billion and that it is correct not to classify uncompensated expenditures for ME1 and ME3 as “inadmissible state aid”, as claimed since 2014. Comparison with Poland is also relevant in this context. Poland made the notification before the privatisation of the coal-fired power plants. In Bulgaria, the agreements were a fact and in line with EU policies.

The 2014 demarche to the EC for “State aid” for ME 1 and ME 3 is pointless at least because the applicants themselves set cross subsidies to other players of the electricity system, such as the cogeneration capacities of the district heating companies, and the so-called factory plant power plants, and more recently Varna TPP has been added to them. It is strange that in the numerous attacks against the “American” TPPs, no attention is paid neither to the factory power plants (before) nor Varna TPP (now).

Historical overview and state of affairs

ME1 and ME3 are intended as a replacement for the small four reactors of Kozloduy NPP (a condition for EU membership due to the requirement for security, risk-free operation, etc.). The government then informs the EU that it does not accept the condition for shutting down these reactors. (Only later, in 2002, the government takes a decision to close them.) In 1999, however, there is a challenge with the old power plants. To address this situation, in 1999, a decision was made to invest privately in two modern local power plants, using local resources such as lignite, to modernise the technological base and the ecological footprint of energy, in which, apart from Kozloduy NPP, there has been no update since the mid-1960s.

Negotiations for a low-interest loan with a long grace period from the Japan Bank for International Cooperation began in 1999 for the state-owned ME2 TPP. It was ratified by parliament in early 2004 and amounts to almost Yen 30 billion (EUR 217 million, 15% of which are Bulgarian government loans), granted at 2.78% annual interest. (At this time, the Bulgarian government cannot take new loans at less than 8%.) It is also envisaged that ME2 and Kozloduy NPP are the only base facilities to remain state-owned. The only possible way to finance the renovation of ME3 and the construction of a new ME1 is to conclude long-term power purchase agreements. What is the reason? Quite simply, in 2001 the interest rate on Bulgarian government bonds was 14.8%, as we wrote with my colleague Bogdanov at the time.

Since 2001, the rationality of this approach has been confirmed by seven Bulgarian governments and two energy strategies. I do not know an energy expert or Minister of Energy since 1998, who thinks that the closure of the Maritsa East TPPs is a necessary and hassle-free undertaking. Meanwhile, the “American” TPPs are much more transparent and competitive, having better economic and environmental performance than their ‘Bulgarian’ counterparts.

It is strange that in 2020 representatives of the private sector of the economy plead for nationalisation of other private sector representatives. Traykov, Dilovska and Rashev, and the “so on” experts are right to ask how all investors in Bulgaria would feel if any subsequent government could expropriate, cancel, terminate already concluded agreements just because they were “unprofitable” according to some of the competition. There is no doubt that such behaviour would keep away foreign investors from Bulgaria for a long time, if not forever.

* Analysis by Krassen Stanchev for Trud Daily